Let me show you something uncomfortable.

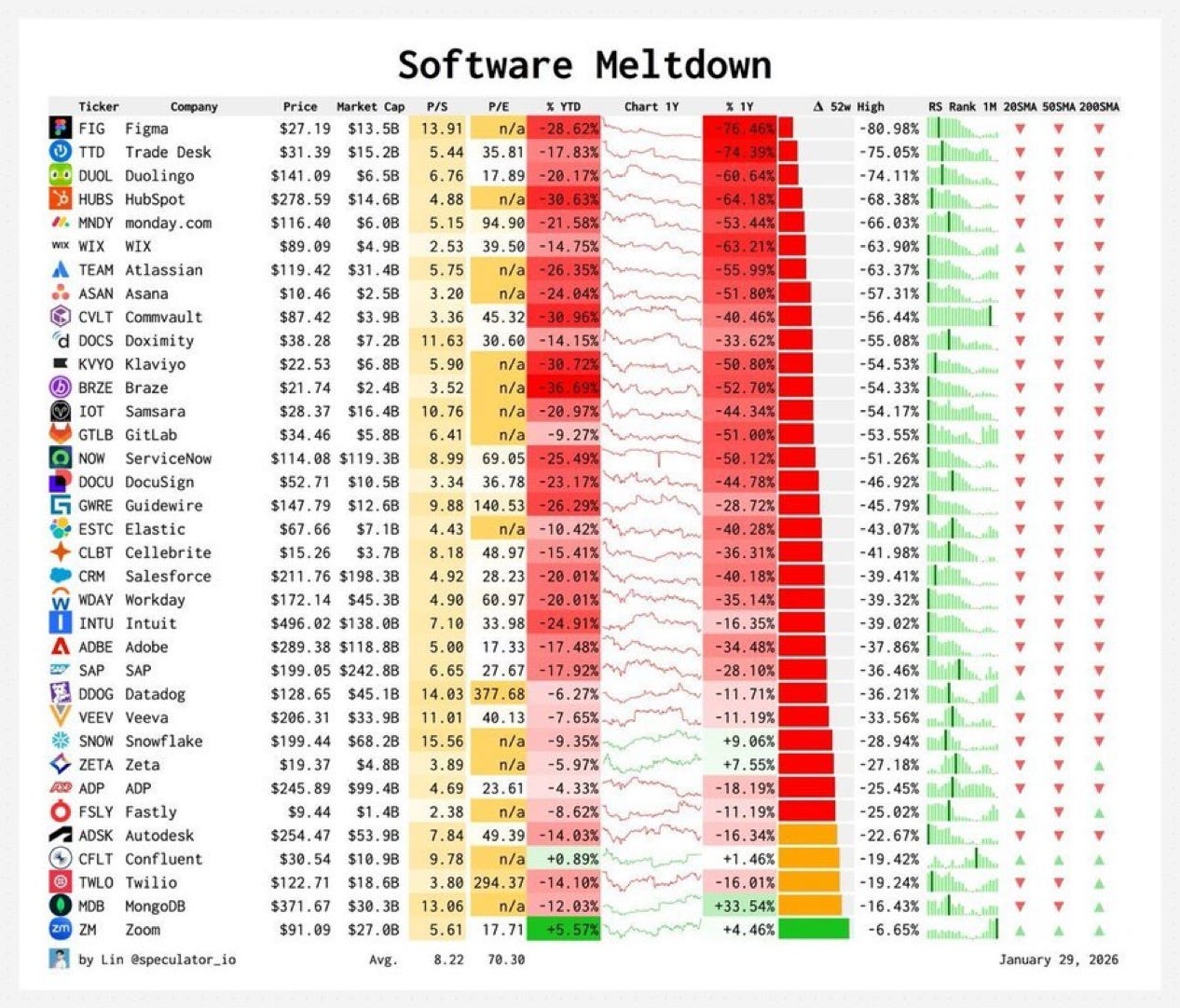

Pull up almost any SaaS stock chart right now. Scroll through the list. Figma down 76% from its 52-week high. Trade Desk down 74%. Duolingo. HubSpot. Monday. Atlassian. The names go on and on—and almost every single one is a bloodbath.

Someone shared a “Software Meltdown” tracker on Twitter recently—35+ public SaaS companies, neatly arranged in rows of red. Over 90% of them are trading 30-80% below their highs. Not their all-time highs from 2021. Their 52-week highs. We’re not talking about a hangover from pandemic valuations. This is a fresh wound.

And I keep seeing smart people treat this like a blip.

It’s not a blip.

What the Numbers Actually Tell You

Here’s the thing about financial tables like this one—they’re a Rorschach test. You see what you want to see.

Optimists look at this and say: “Overblown. Markets overcorrected. These are great businesses at discount prices.”

Pessimists look at this and say: “SaaS is dead.”

I look at this and see something in between—but much closer to the pessimist end than most operators want to admit.

These aren’t bad companies. ServiceNow is a generational business. Salesforce built the modern CRM category. Datadog is genuinely excellent infrastructure. These are not fly-by-night SPACs.

And yet: -50%, -40%, -39%. Across the board.

The market is saying something. The question is whether we’re actually listening.

The Business Model Problem Nobody Wants to Name

Here’s my read: the SaaS business model as it was designed is getting stress-tested in real time—and a lot of these companies are failing the test.

The classic playbook looked like this: charge a per-seat subscription, grow revenue by adding seats, expand within accounts by adding modules. Land, expand, retain. Print money forever.

It worked beautifully for about fifteen years.

Then a few things happened simultaneously.

First, buyers got exhausted. The average mid-market company now has 130+ SaaS tools. Nobody knows who’s using what. Finance is running audits. CFOs are cutting anything that can’t prove ROI in a single quarter. The “expand” motion hit a wall.

Second, the macro tightened. When money was free, growth-at-any-cost was the game. Investors rewarded forward multiples. Now they want cash flow. That shifted the entire incentive structure of how these companies operate—and the best ones are adapting fast, but most aren’t.

Third—and this is the one I watch most closely—AI entered the building.

And it’s not leaving.

The AI Tax on Traditional SaaS

I want to be careful here because this argument gets oversimplified constantly.

“AI will kill SaaS” is too reductive. But “AI won’t change the SaaS business model at all” is delusional.

Here’s what I actually believe: AI is applying a structural tax on seat-based SaaS.

Think about it practically. If I can deploy an AI agent that does the work of three SDRs, why am I paying for three SDR seats in my CRM? If I can use AI to automate reporting, why do I need five analysts licensed in my BI tool?

The headcount-to-software relationship is breaking down. And a huge chunk of SaaS revenue is anchored to headcount.

This isn’t hypothetical. It’s already showing up in net revenue retention numbers. Companies that were at 120%+ NRR are sliding back toward 100%. Some below. The expansion motion that powered the entire growth thesis for this category is slowing in real time.

The Survivors vs. The Casualties

Not all of these red numbers are the same story.

There’s a difference between companies that are going through painful repricing and companies that are facing genuine existential pressure.

Look at Zoom—down only 6.65% from its 52-week high in this dataset. Zoom rebuilt itself. They moved aggressively into AI, rethought the product surface, and accepted that they’d never recapture their pandemic multiple. That’s discipline.

MongoDB is up 33% over the last year. Snowflake has a positive year. Confluent is basically flat.

Notice anything about those names? They’re infrastructure. Data and developer tools. Not workflow automation, not productivity apps, not feature-software that AI can increasingly replicate.

The pattern here is pretty clear if you’re willing to see it: software that sits below the workflow—in the data layer, the infrastructure layer, the integration layer—is holding up better than software that sits in the workflow.

Because AI is eating workflows. It’s not yet eating the pipes that data runs through.

What This Means for You

If you’re an operator, you need to make two kinds of bets right now.

Bet one: Audit your stack ruthlessly. If you’re paying for SaaS seats that deliver outputs AI can now produce—automate, consolidate, or cut. Your competitors who are doing this are getting structural cost advantages you can’t close with hustle.

Bet two: Think hard about which tools in your stack have infrastructure leverage. The SaaS products that own your data, your integrations, or your core operational record are defensible. The ones that own workflows—especially repeatable, language-based workflows—are not.

If you’re in SaaS, building SaaS, or selling SaaS, the question you should be asking isn’t “how do we add AI features?” It’s “does our product live above or below the AI automation line?”

That question will determine whether your company ends up in the red column or the green one over the next three years.

A Final Thought

I’ve worked in and around technology long enough to have seen a few of these cycles. The dot-com crash. The 2008 correction. The 2022 SaaS repricing.

Every time, two things happen.

The majority of people insist this is temporary. And then a meaningful portion of the incumbents don’t make it through—not because they weren’t good businesses, but because they couldn’t adapt fast enough to a structural shift that was actually happening.

This feels structural to me.

The companies that make it out the other side will be the ones that got honest about it early.

Are we being honest yet?