Half a Trillion Dollars Moved in a Day. Here’s What Nobody’s Talking About.

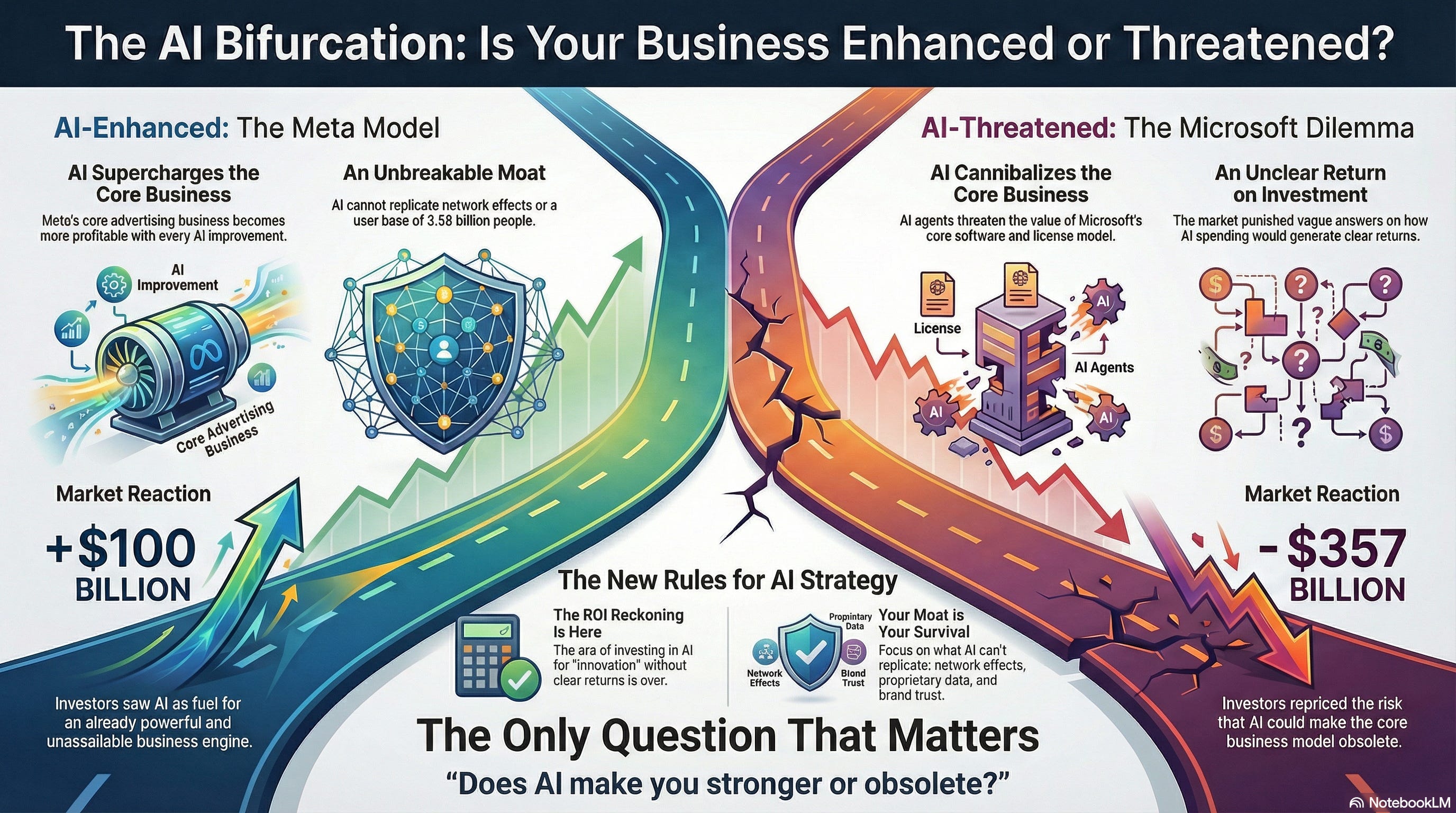

Microsoft announces $80 billion in AI spending for the year. Stock tanks 10%. $357 billion in market cap—gone.

Microsoft announces $80 billion in AI spending for the year. Stock tanks 10%. $357 billion in market cap—gone.

Same day. Same announcement type.

Meta announces roughly the same AI investment. Stock rips 10%. $100 billion added to market cap.

Nearly half a trillion dollars swung between two companies in 24 hours. Both spending fortunes on AI. Both considered tech giants. Both led by people Wall Street generally trusts.

The difference? One is seen as building the future. The other is seen as fighting for survival.

I’ve spent the last week digging into this, talking to investors, and thinking about what it means for every company betting on AI right now. What I found isn’t just interesting—it’s a fundamental shift in how the market values technology companies.

And if you’re leading any kind of AI initiative, you need to understand this.

The Numbers Don’t Lie (But They Don’t Tell the Whole Story Either)

Let me show you the tale of the tape:

Microsoft beat revenue estimates. Cloud revenue grew 39%. That’s still incredible growth for a company this size. But guidance came in soft on personal computing, and Azure growth was a hair below expectations.

Meta posted 24% year-over-year revenue growth. Q1 guidance came in ahead of analyst consensus. Their core business is absolutely humming.

Both announced AI spending in the $65-80B range for 2026. Similar scale. Similar ambition.

Completely different market reactions.

Here’s what struck me: This wasn’t about how much they’re spending on AI. It was about what happens to their core business because of AI.

And that distinction matters more than anything else happening in tech right now.

The Question Wall Street Is Actually Asking

There’s a thesis circulating among institutional investors that I keep hearing. Ben Reitzes at Melius Research put it most bluntly: “AI is eating software.”

Think about that for a second.

The very tools these companies are building—the code-generation systems, the agent frameworks, the automation platforms—they’re threatening the business models that fund their development.

I see this every day. We’re deploying Care Agent across thousands of clinics, and what we’re building doesn’t just make the existing software more efficient. In many cases, it replaces what the software was supposed to do.

This is the existential question facing every software company: Is the AI you’re building going to strengthen your moat, or flood it?

Two Companies, Two Completely Different Bets

Let me break down why the market sees these two companies so differently.

Meta’s position is actually pretty simple.

Their core business is advertising. 97% of revenue. The thing about advertising is—AI makes it better. Every dollar Meta spends on AI improves ad targeting. Better engagement. Higher revenue per user. More precise attribution.

And here’s the kicker: You can’t use AI to generate 3.58 billion daily active users. You can’t prompt your way into network effects. Meta’s moat isn’t software. It’s people. Attention. Habit.

So when Meta spends $80 billion on AI, the market sees it as pouring fuel on an already-powerful engine. If their big AI bets fail? They still have the dominant advertising platform on the planet. Worst case, they’re back to running an insanely profitable business.

That’s called “upside optionality on an unassailable foundation.”

Microsoft’s situation is... more complicated.

Their core business is software and cloud. Windows. Office. Azure. Enterprise licensing. The business model that built the modern software industry.

And that’s exactly what AI threatens.

Think about it. If Claude Code (or Copilot, or any of these tools) can write, debug, and maintain software—why do you need as many seats? Why pay for licenses when an agent can perform the function?

Microsoft’s CFO Amy Hood basically admitted they prioritized GPU resources for internal Copilot projects over Azure customer growth. Let that sink in. They’re spending billions on internal experiments while constraining their most profitable business line.

When analysts asked about ROI on all this AI spending, the answers were... vague. The market noticed.

The Valuation Framework Has Changed

Here’s what I think is really happening.

For decades, software companies were valued on what’s called “terminal value”—the assumption that the business will generate cash flows basically forever. High recurring revenue. Low churn. Predictable growth. The SaaS model that everyone copied.

AI breaks that assumption.

If an agent can replicate what your software does, your terminal value approaches zero. Not immediately. But fast enough that investors are repricing the risk now.

Look at what happened the same week. ServiceNow beat earnings. Raised guidance. Stock dropped 10%. SAP missed slightly. Stock cratered.

The old playbook—hit numbers, raise guidance, get rewarded—it’s gone. Now the only question that matters is: “Does AI make you stronger or obsolete?”

Morgan Stanley put it perfectly: “Good, but not good enough” is the new standard.

What This Means If You’re Building With AI

I’ve been thinking about this through the lens of what we’re building at Experity and what I’m seeing across the companies I advise. A few things stand out:

First: You need to know which side of the bifurcation you’re on.

Every company is now either AI-Enhanced or AI-Threatened. There’s no middle ground. No “we’ll figure it out” position that the market will tolerate.

AI-Enhanced means your core business—the thing that generates most of your revenue and profit—gets stronger when AI gets better. Your moat widens. Your unit economics improve. Your competitive position strengthens.

AI-Threatened means AI can replicate your core value proposition. Maybe not today. But soon enough that smart investors are pricing it in.

Be honest about which camp you’re in. Because the strategy for each is completely different.

Second: The ROI reckoning is here.

The era of “we’re investing in AI for innovation” without clear returns? It’s over. Done.

When Microsoft can’t articulate why their AI spending will generate returns, and the market punishes them by $357 billion, everyone notices.

If you’re making AI investments, you need to show how it enhances your existing profitable business lines. Not hypothetical future revenue. Not “optionality.” Actual, demonstrable return on the capital you’re deploying.

Third: Moats matter more than ever.

In a world where AI can replicate functionality, what can’t it replicate?

Network effects—the kind Meta has with billions of users. Proprietary data that gets better the more you use the product. Regulatory capture. Brand trust built over decades.

I think about this constantly with Care Agent. The 2.5 million conversations we’ve handled aren’t just volume. They’re training data. They’re understanding of how patients actually communicate about their health. They’re insights into clinical workflows that no one else has.

That’s a moat AI builds, not threatens.

Fourth: Your software vendors are facing a crisis.

This has immediate practical implications. The companies you buy software from are fighting for survival. Expect desperate pricing. Expect aggressive pivots. Expect some of them to disappear.

This creates opportunity—you’ve got leverage in negotiations you didn’t have a year ago. But it also creates risk. That vendor you’re deeply integrated with? Their roadmap might look very different six months from now.

The Brutal Math of the New Era

I want to leave you with one thought.

Microsoft and Meta both bet their futures on AI. Both committed enormous resources. Both have incredibly smart people leading the charge.

But only one convinced the market that their core business survives to enjoy the rewards.

That’s the brutal math of this new era. It’s not enough to invest in AI. It’s not enough to build impressive technology. It’s not enough to have a vision for the future.

You have to answer one question convincingly: Does AI make your business stronger, or does it make your business obsolete?

Microsoft couldn’t answer that question on January 29th. And half a trillion dollars moved in response.

What’s your read? Is your company AI-Enhanced or AI-Threatened? I’m genuinely curious how people are thinking about this.

Hit reply or drop a comment. I’ll engage with the best responses in next week’s analysis.

Didn't expect this take on the market, but it's incredibly insightful. You always mange to find the underlying story, similiar to your piece on tech perception last month.